Payment reconciliation is a crucial process that every company, regardless of size, needs to perform regularly. It provides information on a business’s financial health and establishes financial transparency.

Today’s businesses process many financial transactions, making payment reconciliation a challenge for accounting departments. This is especially true in the ecommerce industry, which has adopted the omnichannel strategy. Keeping track of payments that occur via multiple sales channels requires new, automated solutions.

In this article, you will learn about the importance of payment reconciliation, payment reconciliation best practices, and the most common mistakes businesses make.

What Is Payment Reconciliation?

Payment reconciliation is the process of comparing bank statements with accounting documents to make sure they are consistent and up to date. It aims to discover mistakes in balance sheets and resolve discrepancies that come up in finances.

Detecting financial discrepancies through payment reconciliation is essential for avoiding bookkeeping ledger errors and identifying fraud. It is also a good way to follow up on overdue or failed payments.

Note: If you own a US-based ecommerce business, check out our guide for best ecommerce accounting practices.

Payment reconciliation is demanding and time-consuming but must be performed regularly. Depending on the business size, conduct payment reconciliation daily, weekly, monthly, or quarterly.

There are two types of payment reconciliation:

- Personal reconciliation. It compares your personal account statements with receipts. Smartphone banking apps simplify this process by sending notifications to users about their account deposits and withdrawals.

- Business reconciliation. It includes comparisons of financial documents across multiple accounts and sectors of the company. Business reconciliation is complex and often requires the assistance of third parties, such as accounting firms. The process is essential for taxes, as these are based on company’s assets and sales.

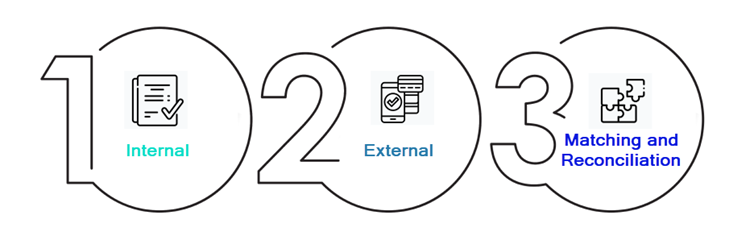

Payment Reconciliation Process

There are 3 stages of the business payment reconciliation process.

1. Internal

Internal data extraction is the first stage of business reconciliation. During this stage, internally retrieve documents on financial transactions performed in the given period (within the company). This includes the accounting documents that the company stores, whether digitally or on paper.

2. External

The second stage of business reconciliation involves collecting data on external business activities. Collect bank statements relevant to the transactions that were recorded and collected in the previous phase.

3. Matching and Reconciliation

Matching and reconciliation is the central phase of the business reconciliation process. During this stage, compare internal and external documents to find discrepancies.

Report all financial errors for fixing. Most discrepancies are due to mistakes made internally but occasionally the bank is at fault due to a data breach.

Reconciliation goes through several stages of review and approval. This part of the process is the most complex since all detected errors need to be resolved manually. That is why, companies should automate the previous two steps to make this process go as smoothly as possible.

After reconciliation is completed, the updated data is added to the company’s database.

Why Is Payment Reconciliation Important?

Here are the reasons why businesses need to perform regular payment reconciliation:

- Uncovering and correcting errors. Mistakes happen, but the goal is to uncover financial discrepancies sooner rather than later. Payment reconciliation helps to detect if any of the financial records do not match so you can find their source and correct them.

- Preventing fraudulent activities. Security is very important in any business, and this is true for both merchants and their customers. By performing regular payment reconciliation, a business ensures that its finances are up to the standards of accounting and regulatory bodies, leaving less room for possible fraud.

Note: To prevent payment fraud, the Payment Card Industry Security Standards established a set of rules with which any business receiving card payments needs to comply. For a complete list of merchant compliance requirements, refer to our PCI Compliance Checklist for Merchants.

- Making smart business decisions. Payment reconciliation provides insight into every deposit, withdrawal, failed or overdue payment. This helps a company make informed financial decisions and optimize its spending.

- Preventing extra fees. Payment reconciliation resolves issues with overdraft fees and bounced checks for payments that have not gone through, giving stakeholders an accurate picture of the company’s financial data.

Payment Reconciliation Best Practices

Below is a list of payment reconciliation best practices:

- Automate the reconciliation process. Automation helps save time, especially if payment reconciliation includes huge amounts of financial data. Also, it eliminates the chances for human error.

- Standardize payment reconciliation. Establish a standardized payment reconciliation process and stick to it. Develop templates and standardized procedures employees can use as guidelines.

- Perform internal checks. Besides adopting automation and standardization, it is crucial to perform regular internal controls to check for difficulties and errors in the payment reconciliation process and to ensure the accuracy of the data.

- Fill in manual gaps. Many companies still do a lot of manual work despite adopting automation. Although manual work is necessary, companies should implement automation wherever possible, especially for lower-scale processes. This enables the accountants to focus on more demanding tasks.

- Prioritize tasks on a risk-based approach. When performing payment reconciliation, identify which accounts demand more attention based on the amount of risk they pose to your finances if not handled properly. This also includes determining how often accounts should be reconciled.

- Evaluate and optimize. The financial industry is constantly changing and innovating. Regularly check for solutions that help streamline the payment reconciliation process.

Common Payment Reconciliation Mistakes

These are the most common mistakes in payment reconciliation:

- Not performing payment reconciliation regularly. Perform payment reconciliation on a regular basis, especially if you are running a big business with large transaction volumes.

- Having multiple systems for tracking and storing financial information. Errors proliferate when companies keep their receipts and bank statements in a variety of forms, spreadsheets, or programs instead of in one centralized database.

- Having incomplete data about transactions. This includes proof of financial transactions that lack essential information, such as the date of the transaction or its status.

Conclusion

By performing regular checks and updates of financial documents through payment reconciliation, businesses gain a better insight into their earnings and spending. In addition, payment reconciliation is an essential fraud-prevention tool and gives a business financial transparency.

Payment reconciliation is the cornerstone of sound bookkeeping practices. It gives stakeholders an understanding of the company’s financial health and ultimately contributes to its growth potential.