Introduction

Electronic payments are an essential part of every ecommerce experience. Merchants and their consumers like using payment cards, mobile wallets, and other electronic payment methods because of their speed, security, and efficiency.

However, electronic payments sometimes get declined for a variety of reasons. It is important to determine exactly why this happens to ensure an uninterrupted cash flow for the business and smooth payment processing.

In this article, learn about the difference between soft declines and hard declines, the reasons they happen, and how to prevent them.

Soft Decline vs. Hard Decline: Main Differences

Soft declines are temporary and happen because of an error or technical issue, despite the issuing bank approving the payment. The payment can be retried after the requirements are met (for example, after a cardholder inputs the correct payment card information).

A hard decline is permanent and occurs when the issuing bank rejects a payment. This payment cannot be retried as it will get rejected every time.

Note: Issuing banks and acquiring banks play crucial roles in payment processing. Learn all about them in our article Issuer vs. Acquirer: What Is the Difference?

Soft Decline: An Overview

A soft decline occurs when an issuing bank approves an electronic payment, but an error happens at some point during the payment process. These are the common reasons for a soft decline:

- Incorrect cardholder information

- Card limit exceeded

- Unusual purchase

- Card used abroad without notifying the issuing bank

- Expired card

- IP and billing address mismatch

- Technical or system failure

Merchants can prevent soft declines by enforcing Strong Customer Authentication (SCA). SCA requires customers to provide at least two forms of authentication to verify their identity during payment authorization. This can also help merchants avoid payment fraud and other attempts of abuse of their ecommerce policies.

Soft declines can also be reduced by partnering with a reliable payment processor that has developed the tools to reduce online payment failures, while ensuring payment safety and a smooth user experience.

Example of a Soft Decline

A customer authorizes a payment by inputting the payment information into the payment gateway. However, the payment processor rejects the payment because the authorization request did not pass the card validation code (CVC) or card verification value (CVV) check.

The most likely reason for this is that the customer made a mistake inputting the correct CVC/CVV given on the back of their payment card. The transaction will be settled after the customer inputs the correct information.

Note: Merchants can learn how to differentiate credit card decline codes in our Comprehensive List of Credit Card Decline Codes.

Hard Decline: An Overview

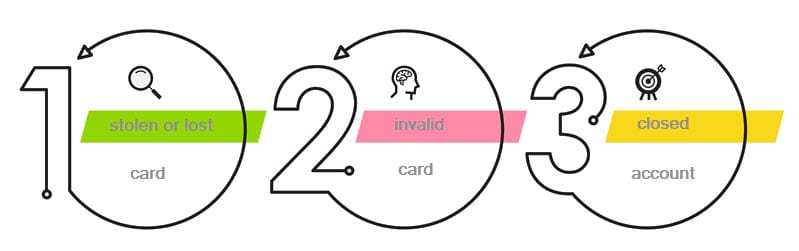

A hard decline happens when an issuer rejects the electronic payment request for security reasons. These are the common reasons for a hard decline:

- Stolen or lost card

- Invalid card

- Closed account

Hard declines cannot be remediated. When an issuer gives a hard decline, the payment cannot be retried since those attempts will also result in automatic rejections. The only solution is to try a different payment card or another electronic payment method.

Example of a Hard Decline

A customer inputs the payment information into the payment gateway during a purchase to authorize the payment. The payment processor sends the merchant a decline message stating the card is reported lost or stolen.

All future payment attempts with this card will be rejected by the issuer, so it is not recommended to retry the payment. Merchants may ask the customer to complete the payment using another method. The customer will have to contact their bank to settle the issue.

Conclusion

Electronic payments sometimes get rejected, and understanding the reasons behind those rejections helps to ensure future uninterrupted payment processing. This also assist merchants and their consumers in resolving issues that result in payment declines and helps prevent them from happening again.