Effective payment processing is one of the main prerequisites for merchants to grow their businesses continuously. As the number of payments made online grows, the need for payment processing is on the rise.

Merchants need to properly understand how payment processing works and what elements it includes to know how to choose a payment processor that is right for them.

In this article, we’ll explain how payment processing works and define the role of each payment processing participant.

Note: Read more in-depth about payment processing in our post What Is a Payment Processor.

Main Payment Processing Participants

Payment processing involves authorized participants which work together to complete an offline or online payment.

Cardholder

A cardholder is an individual who receives a debit or credit card from an issuing bank and opens an account linked to that card. They use the card and/or the account to pay for items or services.

Cardholder's Bank

The cardholder’s bank verifies that their client is eligible to become a cardholder and use a credit or debit card. It is also known as the issuing bank.

Merchant

A merchant is an individual or a company that sells commercial items or services. If this entity sells those goods on the Internet, they’re referred to as an ecommerce merchant.

A merchant uses a merchant account to receive funds from payment card transactions. A merchant account is provided to the merchant by their acquiring bank.

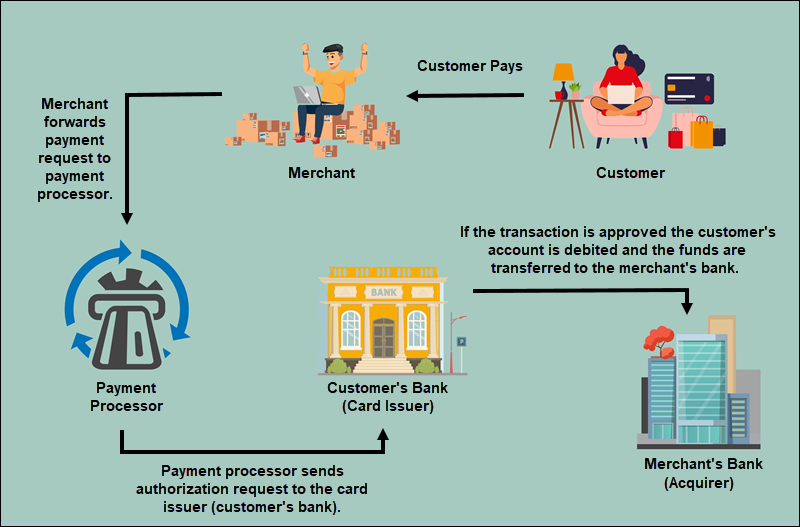

When a buyer pays for the purchased goods, the merchant sends the payment information to their acquiring bank. It forwards it to the card holder’s issuing bank via a card association network. If the payment information is accurate and there are enough funds in the buyer’s account, the issuing bank accepts the transfer of funds from the buyer’s account to the merchant account.

If the buyer pays for goods or services through a digital wallet, such as Google Pay, Apple Pay, or any other similar payment method, the merchant submits the transaction information to the wallet operator. Those data are then forwarded to the payment processor, acquiring bank, and other relevant parties.

Note: Refer to our post Merchant Account Vs. Payment Gateway to learn about all the differences and what each of these can do for you.

Merchant's Bank

Also known as an acquiring bank, a merchant’s bank is a financial institution through which a business organization opens a merchant account, and which maintains that account.

This bank accepts payments via credit and debit cards and forwards them to the merchant account.

Payment Processor

A payment processor is a company that processes offline or online credit card transactions via payment gateways. It mediates between merchants, card networks, merchant banks, and other relevant parties to complete card payments. Every payment processor must ensure that its payment processing procedures comply with the Payment Card Industry (PCI) standards.

Note: PCI compliance includes adhering to operational and technical standards to protect and secure credit card information that card holders submit for credit card payments.

Payment Gateway

A payment gateway encrypts and transmits the buyer’s credit card information to the payment processor. It is a digital passage that enables online communication between the issuing bank and the acquiring bank.

Note: Read our article to better undestand the differences between a payment gateway and a payment processor.

Card Associations

Card associations are financial associations, including MasterCard, American Express, Discover, and Visa. Card associations establish qualification guidelines, interchange rates, and transaction terms for all participants in payment processing.

They are mediators between issuing banks and merchant's banks in case of any disputes.

The Stages of Payment Processing

Payment processing companies implement several stages of payment processing in accordance with strict regulation. Not only do the payment processing stages below guarantee a high level of security during the transaction, but they also ensure that the payment is processed in a timely manner.

Note: Learn how long a credit card payment takes to process.

Authorization

Authorization verifies that every party in a payment processing procedure is entitled to participate in it.

It consists of the following stages:

- The cardholder provides the credit card number to a merchant to pay for purchased goods or services. Online payment requests are carried out via a payment gateway. On the other hand, brick-and-mortar stores use point-of-sale (POS) terminals to accept such payment requests.

- The merchant forwards the payment request to get authorization from their arranged payment processor. If the buyer pays for goods or services through a digital wallet, such as Google Pay, Apple Pay, or any other similar payment method, the merchant submits the transaction information to the wallet operator. The data is then forwarded to the payment processor.

- The payment processor delivers the transaction request to the relevant card association, with the issuing bank as the endpoint.

- The issuing bank receives the authorization request containing the elements of the credit card used in the transaction, such as the card verification value (CVV), the expiration date, and the address verification services (AVS).

- The issuing bank either rejects or confirms the transfer. The transaction may be declined for the following reasons: insufficient funds on the credit card, payment date has passed, or the cardholder’s account is invalid or has expired.

- The approval or denial notification is sent by the issuing bank to the card association, the merchant bank, and, eventually, the merchant.

Thanks to advanced payment technologies, authorization is usually completed within several seconds or minutes.

Note: Canceled transactions are a common occurrence in the world of merchants. Learn everything you need to know about void payments i.e. void transactions.

Settlement and Funding

Settlement is the final stage of payment processing, during which the merchant receives the amount of money that the customer paid for the purchased goods or services. Payment processing participants handle settlement and funding in the following way:

- The merchant sends a batch of authorized payments to the payment processor.

- The payment processor forwards the transaction data to the card association.

- The card association notifies the relevant issuing bank within their network of the requested debit.

- The issuing bank debits the cardholder’s account with the requested amount for the payment.

- The requested funds are then transferred to the merchant bank by the issuing bank. Interchange fees are paid at this stage.

- The merchant bank credits the merchant account with the funds in question.

Credit Card Interchange

Credit card interchange refers to the settlement and clearing of payment data, in which the acquiring bank completes the approved card payments for its merchant. This term refers to costs and fees paid by the acquiring bank to the issuing bank for the performed transaction, as well.

Note: Learn everything you need to know about credit card processing fees for merchants.

Conclusion

Merchants need to consider all payment elements and participants to ensure fast and secure payment processing. By understanding how payment processing works, merchants are less likely to face unwanted chargebacks.